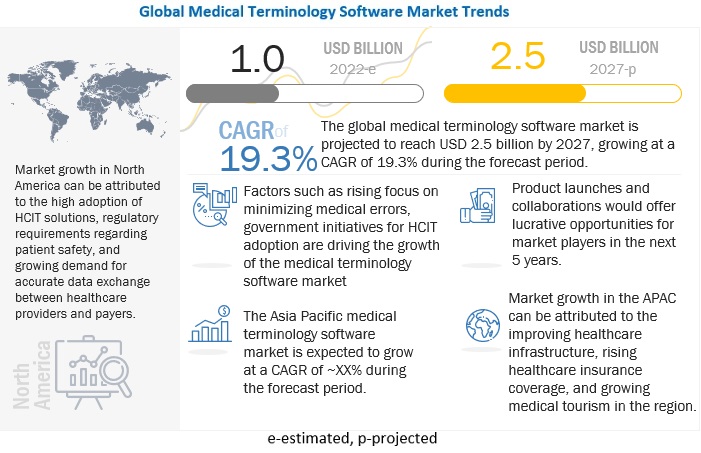

Medical Terminology Software Market worth $2.5 billion by 2027 – Exclusive Report by MarketsandMarkets™

The key factors propelling the growth of this market are growing government initiatives to support HCIT solutions such as medical terminology software and a growing focus on rectifying medical errors. On the other hand, reluctance to use medical terminology solutions is challenging the growth of the global market to a certain extent.

Currently, healthcare ecosystems are quite fragmented in terms of content and infrastructure. A health delivery organization may manage 40 or more separate IT systems, with each system having its own clinical terminology content and infrastructure.

These terminology silos make it difficult for organizations to leverage isolated clinical data, which impacts downstream activities such as data analytics. The problem further intensifies when a health system seeks to share data with other healthcare partners.

In that scenario, the relevant data resides in numerous isolated systems scattered across multiple healthcare organizations. The lack of a common clinical vocabulary across a magnitude of standalone systems is a key obstacle to national efforts to increase interoperability, transparency, and collaboration within the healthcare system.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=239939409

Browse in-depth TOC on “Medical Terminology Software Market”

74 – Tables

26 – Figures

124 – Pages

The quality reporting segment is expected to witness the highest growth rate in the medical terminology software market, by application

Based on application, the quality reporting segment is expected to register the highest CAGR during the forecast period. Factors responsible for the growth of this segment are the benefits offered by the segment such as improved patient safety, improvements in the quality of care, efficient healthcare services & patient outcomes.

By end user, the private payers segment accounted for the largest share of the medical terminology software market, by healthcare payers in 2021.

The private payers segment is estimated to have the largest share by healthcare payers end user of the market. The large share of the segment is attributed to the advantages offered to the private payers such as benefits of normalization through fully integrated medical terminology management solutions to ensure more effective communication, less inconsistency, and more streamlined administrative costs.

Key Players in Medical Terminology Software Market:

- Wolters Kluwer N.V. (Netherlands),

- 3M (US),

- Intelligent Medical Objects, Inc. (US),

- Apelon, Inc. (US),

- Clinical Architecture, LLC (US),

- CareCom (Denmark),

- BiTAC (Spain),

- B2i Healthcare (Hungary),

- BT Clinical Computing (Belgium), and

- HiveWorx (Ireland) are the major players in this market.

These companies are majorly focusing on the strategies such as agreements, collaborations, partnerships, and service launches in order to remain competitive and further increase their share in the medical terminology software market.