The Future For Prostate Health Market

The prostate gland (the prostate) is an organ of the male reproductive system. The three most common forms of prostate disease are inflammation (prostatitis), non-cancerous enlargement of the prostate (benign prostatic hyperplasia or BPH), and prostate cancer. Benign prostatic hyperplasia (BPH) is defined as a medical condition affecting men.

It involves the non-cancerous enlargement of the prostate gland. While BPH rarely shows symptoms before the age of 40, the risk of contracting BPH increases with age. The condition affects nearly 50% of men between the ages of 51 and 60 and up to 90% of men older than 80. Treatment measures such as medications and surgery have been used for patients with BPH.

The incidence of prostate cancer increases with an increase in age. Prostate cancer is the most common type of cancer among men. According to the American Cancer Society’s estimates for prostate cancer in 2021, about 248,530 new cases and 34,130 deaths occurred in 2020 due to prostate cancer in the US. The prostate cancer phase III pipeline is diverse and includes molecules in approved drug classes as well as drugs with novel mechanisms of action, including radioligands targeted to prostate-specific membrane antigen (PSMA), kinase inhibitors, and immune checkpoint inhibitors.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=107055093

The new research study consists of an industry trend analysis of the market. The new research study consists of industry trends, pricing analysis, patent analysis, conference and webinar materials, key stakeholders, and buying behaviour in the market. The prostate gland (the prostate) is an organ of the male reproductive system. The three most common forms of prostate disease are inflammation (prostatitis), non-cancerous enlargement of the prostate (benign prostatic hyperplasia, or BPH), and prostate cancer.

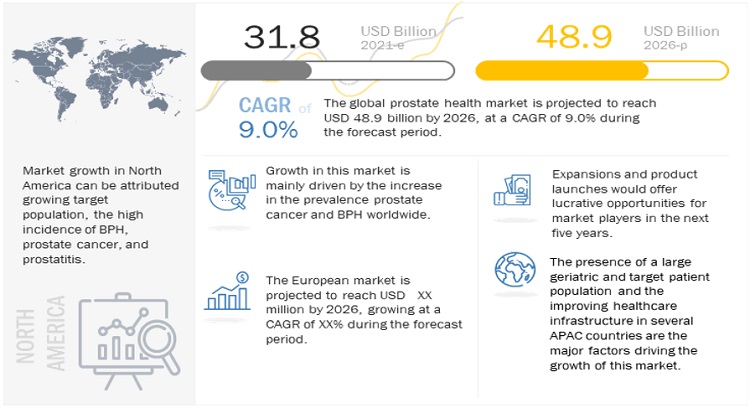

Growth in this market is primarily driven by the increasing prevalence of benign prostatic hyperplasia, increasing obesity, investments, funds, and grants for research in prostate health, an increase in the prevalence of prostate cancer, a surge in demand for hormone therapy drugs, emerging therapies for prostate cancer, and an increasing incidence of prostatitis.

North American prostate health market to dominate the market during the forecast period

North America dominated the prostate health market in 2020 and is expected to grow at an 7.6% CAGR during the forecast period. North America has been among the frontrunners in developing prostate health therapies in the healthcare industry. The market growth in the US (a major contributor to the North American prostate health market) can be mainly attributed to the growing target population, the high incidence of BPH, prostate cancer, and prostatitis, and the strong presence of medical device manufacturers. Additionally, favorable reimbursement policies, high disposable incomes, a strong healthcare infrastructure, research funding, and product launches have accelerated the growth of this market.

Some of the prominent players operating in the prostate health market are Eli Lilly and Company (US), Pfizer Inc. (US), Merck & Co., Inc. (US), GlaxoSmithKline plc. (UK), Abbott (US), and Astellas Pharma Inc. (Japan), and other players.