How The Growing Demand For Healthcare Supply Chain Management Is Transforming The Market

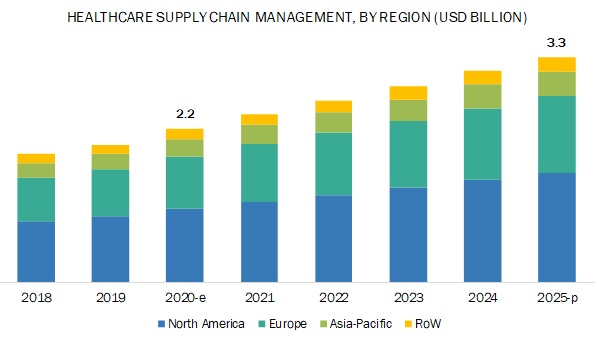

According to market research report, "Healthcare Supply Chain Management Market by Component (Software, Inventory, Order, Warehouse, Purchase, Implant, Transport, Strategic Sourcing, Consignment, Hardware, Barcode, Scanner, RFID), Delivery (On Premise,Cloud), End User - Global Forecast to 2025" The healthcare supply chain management market size is projected to reach USD 3.3 billion by 2025 from USD 2.2 billion in 2020, at a CAGR of 7.9% during the forecast period.

The key factors driving the growth of this market include the adoption of GS1 system of standard in the healthcare industry globally, the emergence of cloud-based solutions, reduction in operational costs by improving the efficacy and increase in overall profitability. However, the high cost of implementation of supply chain management software is expected to restrict market growth to a certain extent.

Healthcare supply-chain management systems are available as two components, software, and hardware. A software system is highly acceptable compared to hardware systems due to the increasing number of online purchases, improving business intelligence, and growing preference for eco-friendly logistics. This is said to enhance the growth of the healthcare supply chain management market in the forecast period.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=77439622

The on-premise segment commanded the largest share of the healthcare supply chain management industry, by delivery mode, in 2019.

Based on delivery mode, the market is segmented into on-premise and cloud-based. The on-premise segment accounts for the largest share of the healthcare supply chain management market. However, the cloud-based segment is expected to register the highest growth over the forecast period. Cloud-based solutions help healthcare organizations share and integrate information from disparate locations; these solutions also offer minimum costs of installation and maintenance. Such advantages are driving market growth in this segment.

Manufacturers are the largest end-users of the healthcare supply chain management market.

Based on the end-user, the healthcare supply chain management industry is segmented into manufacturers, providers, and distributors. In 2019, manufacturers accounted for the largest share of the healthcare supply chain management market. Manufacturers must cater to the increasing demand for products from their end-users. Owing to this, manufacturers mainly look for supply chain management solutions for transportation and warehouse management to ensure faster, more accurate, and more efficient functioning. This has resulted in an increased demand for supply chain management solutions in this segment.

North America dominates the healthcare supply chain management industry during the forecast period.

The healthcare supply chain management market is segmented into North America, Europe, the APAC, and the RoW. Of this, North America accounted for the largest share of the healthcare supply chain management industry in 2019. North America is a well-established and lucrative market for healthcare supply chain management. In this regional market, the US is expected to offer potential growth opportunities to market players in the coming years. This can primarily be attributed to the consolidation of hospitals, rising prevalence of chronic diseases, and growing awareness in the country.

SAP SE (Germany), Oracle Corporation (US), and Infor (US) were the leading players in the healthcare supply chain management market. Other players include McKesson Corporation (US), TECSYS (US), Global Healthcare Exchange (US), Cardinal Health (US), Determine (US), Epicor (US), LLamasoft (US), Manhattan Associates (US), Blue Yonder Group, Inc. (JDA Software) (US), Cerner (US), Jump Technologies (US), LogiTag Systems (US), Harris Affinity (US), Premier (US), Accurate Info Soft (US), Hybrent (US), and Arvato Systems (Germany).