From Cold Chain to Construction: Inside the PCM Upswing

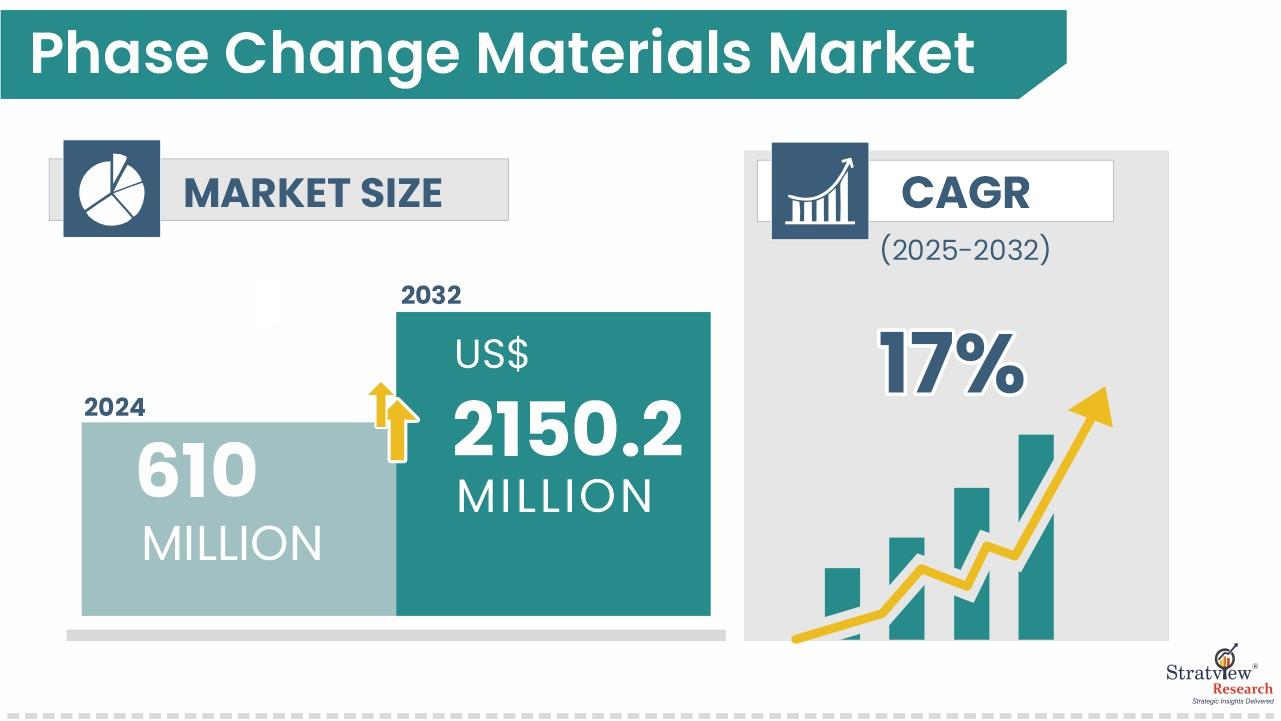

PCMs are engineered “thermal batteries” used across building & construction, HVAC, cold chain & packaging, thermal energy storage, refrigeration & equipment, electronics, textiles, and more. Stratview’s latest read places the phase change materials market at USD 610M (2024), advancing to USD 2,150.2M by 2032 (17% CAGR); an earlier Stratview release projected USD 1,548.3M by 2028 (17.24% CAGR, 2022–2028)—showing consistent momentum across editions.

Download the Free Sample Report:

https://www.stratviewresearch.com/Request-Sample/564/phase-change-materials-market.html#form

Drivers

- Energy and operating-cost pressure. As utilities and owners hunt for demand-side savings, PCMs help shift cooling/heating loads and stabilize temperatures—reducing compressor cycling and peak demand. (Driver framework per Stratview.)

- Quality and safety in logistics. Pharma, biotech, and food operators rely on PCM packs to maintain tight thermal windows during transport and storage, complementing active systems. (Application scope per Stratview.)

- Materials and integration know-how. Availability across inorganic, organic, and bio-based families and encapsulation at macro/micro/molecular scales make PCMs easier to embed in building assemblies, equipment, and packaging lines.

Trends

- Application map. Building & construction remains the largest application, aided by EU building-efficiency directives and retrofit programs; HVAC, TES, and cold chain sustain multi-industry pull.

- Type selection by use case. Inorganic PCMs dominate on conductivity, latent heat, and non-flammability; organics/bio-based are used where cycling behavior, compatibility, or sustainability cues are prioritized.

- Regional dynamics. Europe leads globally; Stratview cites strict building codes and temperature-sensitive goods regulation as key reasons. North America and Asia-Pacific round out demand with varied building standards and logistics growth.

- Ecosystem depth. A mix of chemicals, specialty materials, and cold-chain firms compete—Honeywell Electronic Materials, Laird, Sasol, Croda, Entropy Solutions, Microtek, Pluss, PCES, Rubitherm, Outlast, Henkel, Cold Chain Technologies, and others.

Conclusion

PCMs are moving from niche to specification standard wherever temperature stability and energy savings matter. Expect Europe to remain the bellwether region and inorganic chemistries to carry volume, while encapsulation options enable broader productization. Stratview’s forecasts—USD 1.55B by 2028 and USD 2.15B by 2032—point to a durable, cross-sector growth curve for vendors that can translate material science into validated, field-ready solutions.