Exploring the Impact of Life Science Instrumentation on the Market

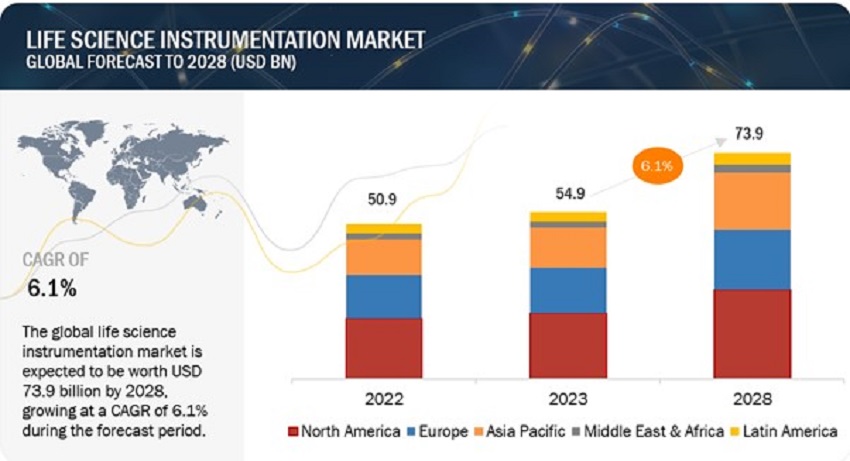

According to latest research report "Life Science Instrumentation Market by Technology (Spectroscopy, Chromatography, Immunoassay, NGS, PCR, Microscopy), Application (Diagnostic, Clinical), End User (Pharma, Agriculture & Food Industry, Hospitals, Diagnostic Labs) - Global Forecasts to 2028", the global life science instrumentation market projected to reach USD 73.9 billion by 2028 from USD 54.9 billion in 2023, at a CAGR of 6.1% from 2023 to 2028.

The pharmaceutical industry focuses and invests in research to manufacture protein-related products. Drug development and manufacturing involve different types of analytical instruments. Analytical instruments evaluate drug molecules, protein analysis and purification, and quality control. Protein identification and separation is an important step in drug manufacturing.

Technologically advanced equipment helps understand the characterization of a molecule and ensure its safety and purity. In recent years, emerging markets have also witnessed a significant increase in foreign direct investment and government investments in pharmaceutical R&D. Thus, increasing R&D spending in the life sciences, pharmaceutical, and biotechnology sectors will likely increase the application usage of life science instruments.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38

Research applications segment accounted for the largest share of the life science instrumentation market, by application in 2022.

Based on application, the global life science instrumentation market is segmented into research applications, clinical & diagnostic applications, and other applications. Research applications accounted for the largest share of the market in 2022 and is expected to grow at the highest CAGR during the forecast period. Factors such as the rising incidence of infectious diseases, the growing use of novel analytical techniques, and the launch of advanced instruments drive the growth of life science instruments.

The pharmaceutical & biotechnology companies segment accounted for the largest share of the life science instrumentation market, by end user, in 2022

Based on end user, the global life science instrumentation market is segmented into hospitals and diagnostic laboratories, pharmaceutical & biotechnology companies, academic & research institutes, agriculture & food industries, environmental testing laboratories, clinical research organizations, and other end users. The pharmaceutical & biotechnology companies segment accounted for the largest share of the market in 2022. Factors such as rising healthcare expenditure and consistent increases in the adoption of advanced instruments by different end users are driving the growth of this segment.

The Asia Pacific market to register the highest growth in the market during the forecast period

The Asia Pacific life science instrumentation market is anticipated to register the highest growth from 2023 to 2028. Major players in the market are focusing on expanding their manufacturing capabilities in the APAC. This region is consistently witnessing a rise in the adoption of analytical instruments, offering significant growth opportunities for the key players.

As of 2022, prominent players in the life science instrumentation market are Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), Agilent Technologies, Inc. (US), Waters Corporation (US), and Shimadzu Corporation (Japan)