Cold Pressed Oil Market Evolution, Demand Patterns, and Forecast Analysis 2035

Overview

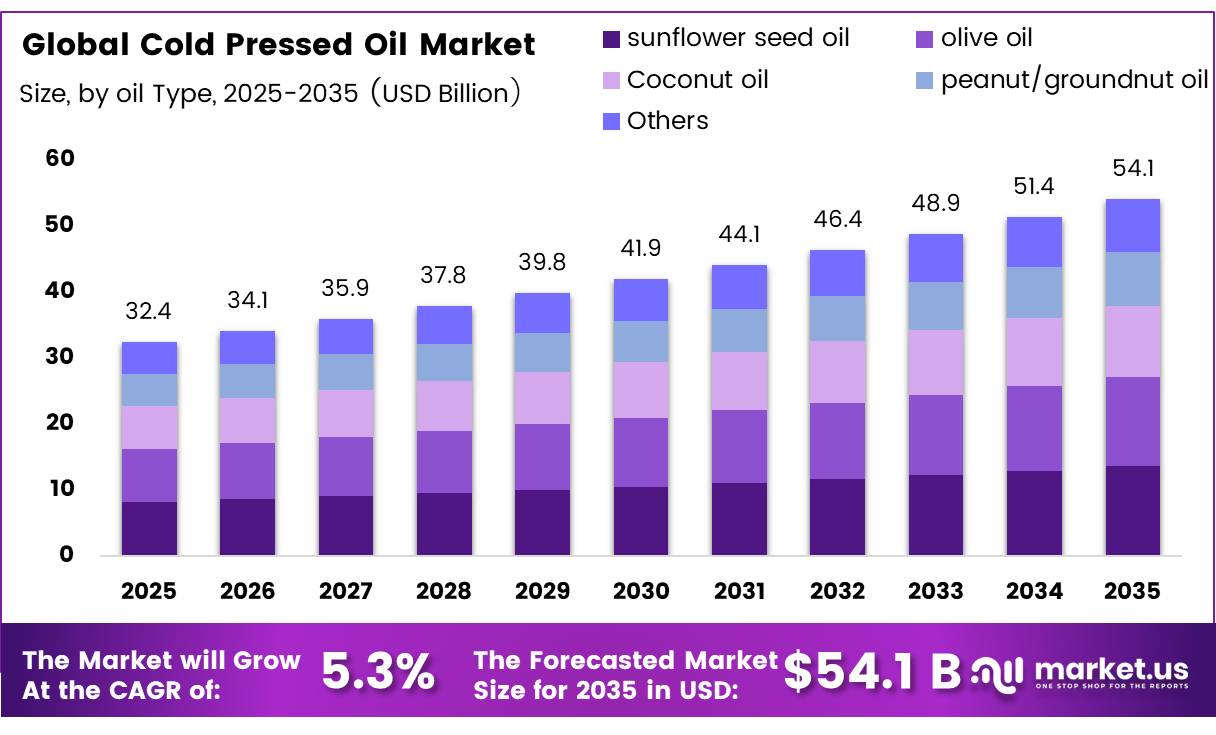

The Cold Pressed Oil Market was valued at USD 32.4 billion in 2025 and is anticipated to reach USD 54.1 billion by 2035, growing at a CAGR of 5.3% over the forecast period. The increasing consumption of premium edible oils and rising awareness about natural extraction processes are contributing to market growth. North America dominated the market in 2025 with a significant 45.6% share, representing revenue of USD 14.77 billion. Growing interest in organic and wellness-oriented products continues to influence consumer purchasing behavior.

Key Takeaways

- The Cold Pressed Oil Market was valued at USD 32.4 billion in 2025 and is expected to grow at a CAGR of 5.3%, reaching USD 54.1 billion by 2035.

- Based on oil type, sunflower seed oil dominated the market with a 30% share due to strong agricultural availability and processing demand.

- By nature, conventional cold pressed oil held a major position with a 55% share, while organic cold pressed oil emerged as the fastest-growing segment.

- Based on end-use application, the Food & Beverage Industry led the market with a 45.2% share due to increasing consumer preference for natural and minimally processed oils.

- Among distribution channels, online retail accounted for a leading 35.6% share, supported by increasing digital purchasing trends.

- In 2025, North America remained the dominant regional market, capturing 45.6% of the total global consumption.

By Oil Type Analysis

Sunflower Seed Oil represents the dominant segment in the Cold Pressed Oil Market, accounting for 30.0% share. Its leading position is supported by the large-scale global cultivation base and continued demand for sunflower oil processing. According to the USDA Foreign Agricultural Service, global sunflower seed oil production stood at 22.12 million metric tons in MY 2023/24, while output reached 20.47 million metric tons in MY 2024/25. Global sunflowerseed crush reached 48.38 million metric tons in MY 2024/25, reflecting sustained processing demand.

Olive oil represented a 25.0% share and emerged as the fastest-growing segment within cold pressed oils. Recovery in global olive oil production and increasing consumer interest in minimally processed oils are supporting segment expansion. Global olive oil production was forecast to reach 3.1 million metric tons in MY 2024/25, recovering from production challenges in previous years. Rising consumption in regions including the European Union and the United States highlights growing demand for premium cold pressed oil products.

By Nature Analysis

Conventional cold pressed oil held the largest market share at 55.0%, supported by the extensive availability of conventionally cultivated oilseeds worldwide. Large-scale agricultural production systems continue to provide raw materials for cold pressed oil processing. The organic cold pressed oil segment is experiencing faster growth due to increasing consumer demand for natural, chemical-free, and sustainable food products. The expansion of certified organic agricultural operations is strengthening the supply base for organic cold pressed oils. Growing interest in organic food consumption is encouraging manufacturers to introduce premium oil products with organic certifications.

End Use Application Analysis

The Food & Beverage Industry dominated the Cold Pressed Oil Market with a 45.2% share. Rising awareness about healthy eating habits and demand for natural ingredients are increasing the adoption of cold pressed oils in households, restaurants, and food manufacturing applications. The Cosmetics & Personal Care segment is the fastest-growing application area. Cold pressed oils are increasingly used in skincare and beauty formulations due to their moisturizing, antioxidant, and skin-nourishing properties. The shift toward plant-based and sustainable personal care products is supporting demand for these oils.

Distribution Channel Analysis

Online Retail dominated the Cold Pressed Oil Market with a 35.6% share, driven by consumer preference for convenient purchasing, product comparison, and access to specialty food products. The continued growth of digital commerce platforms is improving product visibility and availability. Supermarkets and Hypermarkets represent the fastest-growing offline distribution channel. Physical retail formats continue to play an important role in food purchases, allowing consumers to discover and repeatedly purchase premium cold pressed oil products.

Key Market Segments

By Oil Type

- Coconut oil

- Olive oil

- Sunflower seed oil

- Peanut/groundnut oil

- Others

By Nature

- Organic

- Conventional

By End-Use Application

- Food & Beverage Industry

- Cosmetics & Personal Care

- Pharmaceuticals & Nutraceuticals

- Agriculture

By Distribution Channel

- Online Retail

- Supermarkets and Hypermarkets

- Departmental & Convenience Stores

- Specialty Stores

Driving Factors

Growth of Organic and Premium Grocery Channels

The expansion of organic and premium grocery channels is creating additional opportunities for cold pressed oil brands. Increasing availability of premium food products in organic, natural, and wellness-focused retail environments is improving consumer access to cold pressed oils. The United States organic market reached $76.6 billion in 2025, while Germany’s organic sales reached EUR 17 billion in 2024. The growth of organic food markets is strengthening demand for premium, minimally processed products and supporting cold pressed oil adoption.

Rising Demand for Clean-Label and Minimally Processed Foods

Consumers are increasingly choosing products with natural ingredients and fewer processing steps. Cold pressed oils benefit from this trend because the extraction process helps retain natural antioxidants, vitamins, flavor compounds, and bioactive nutrients.

Expansion of E-commerce and Direct-to-Consumer Channels

Digital platforms are improving product discovery and accessibility for specialty edible oils. The increasing adoption of online shopping is helping cold pressed oil brands reach health-conscious consumers across different regions.

Restraining Factors

Feedstock and Edible Oil Price Volatility

Raw material price fluctuations remain a major challenge for cold pressed oil producers. Changes in seed availability, supply disruptions, trade conditions, and production costs can influence pricing and profitability. The FAO Vegetable Oil Price Index averaged 185.0 points in May 2026, reflecting continued market volatility. Rising input costs can increase consumer prices and affect affordability, particularly in price-sensitive markets.

Premium Pricing and Affordability Gap

Cold pressed oils generally carry premium pricing compared with conventional refined oils. This affordability gap can limit adoption among cost-sensitive consumers, especially in emerging markets.

Competition from Low-Cost Refined Oils

Mass-market refined oils continue to create competitive pressure due to lower prices and wider availability. This challenge can restrict cold pressed oil expansion into mainstream consumer segments.

Growth Opportunity

Private-Label Premium Retail Partnerships

Private-label expansion represents a significant opportunity for cold pressed oil producers. Retailers and specialty chains are increasingly seeking premium, organic, non-GMO, and identity-preserved oil products under their own brands. Private-label partnerships can help manufacturers increase production scale, improve plant utilization, reduce marketing expenses, and gain access to premium retail shelves. The opportunity remains significant across Europe, North America, and India’s modern trade, where demand for premium own-brand products continues to increase.