Power Tool Market Key Insights Into Distribution Channel Transformation

Overview

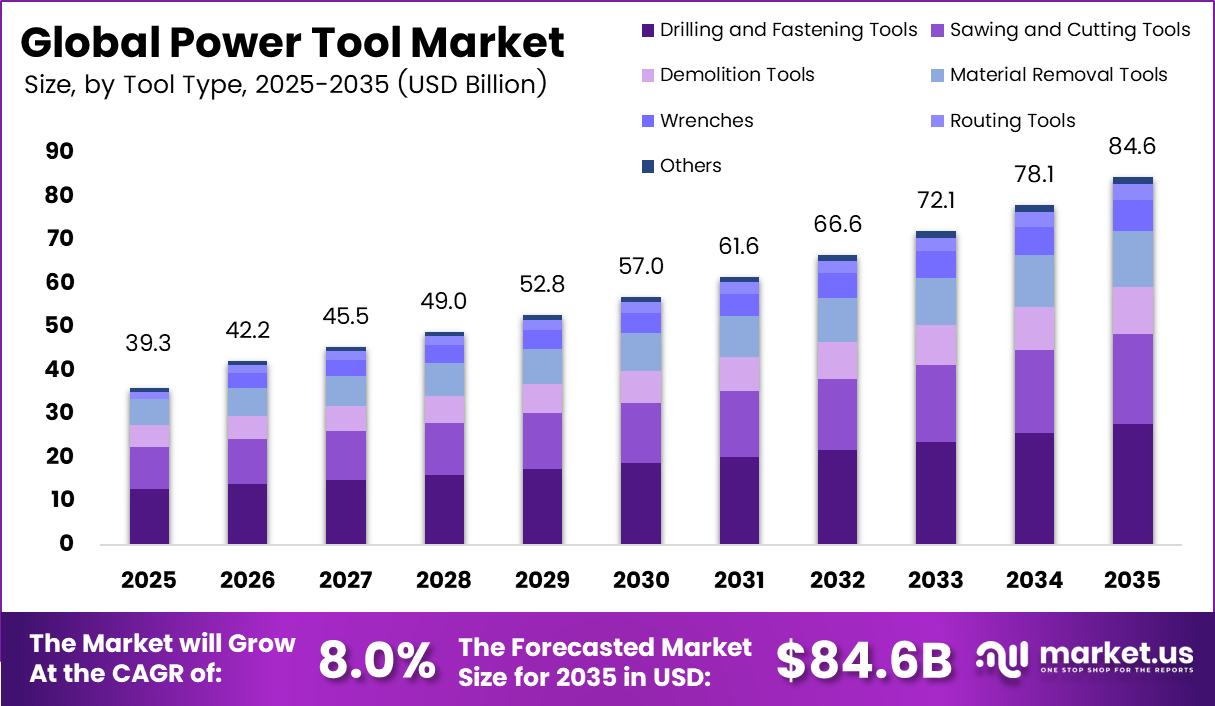

Power Tool Market is expanding rapidly with increasing demand from construction, industrial, and automotive sectors. The market was valued at USD 39.3 billion in 2025 and is forecasted to reach USD 84.6 billion by 2035, growing at a CAGR of 8.0% during 2026–2035. North America contributes 33.0% of the market share, supported by infrastructure investments, manufacturing activities, and technological advancements in cordless and electric tools.

Key Takeaways

- The global power tools market size was valued at US$ 39.3 billion in 2025.

- The global power tools market is expected to register a CAGR of 8.0%, reaching US$ 84.6 billion by 2035.

- By Tool type, drilling and fastening tools accounted for a significant share of the market, representing 32.8% of the overall market share.

- By mode of operation, electric power tools represented a significant market share of about 66.5%

- By application, the industrial/ professional category was a significant share of the power tools market, contributing 68.0% of the overall market share.

- By distribution channel, offline retail was a significant share of the market, contributing approximately 58.0% of the overall revenue share.

- In 2025, North America was a significant share of the global power tools market, contributing 33.0% of the overall market share.

Tool Type Analysis

Drilling and fastening tools represent the dominant segment in the power tools market, accounting for 32.8% share. These tools are widely used across construction, automotive, manufacturing, and maintenance industries due to their precision, efficiency, and ability to reduce manual labor requirements.

The segment continues to benefit from infrastructure development, industrial automation, and increasing demand for advanced equipment. Technological advancements, including wireless tools, lithium-ion battery-powered tools, ergonomic designs, lightweight products, and energy-efficient solutions, are improving productivity and convenience across professional and residential applications. The growing adoption of wireless drills and fastening tools at construction sites and automobile manufacturing facilities is further supporting segment growth.

Mode of Operation Analysis

Electric power tools dominate the market by mode of operation, accounting for approximately 66.5% of the overall market share. Their leadership is supported by high operational efficiency, easy handling, lower maintenance requirements, and extensive applications across industrial, commercial, construction, automotive, and residential sectors.

Cordless drills, impact drivers, angle grinders, and rotary hammers equipped with lithium-ion batteries are increasingly preferred due to their portability and performance advantages.

Pneumatic power tools account for 18.6% of the overall market share and remain important in heavy-duty industries because of their reliability and high performance. However, their dependence on air compressors and complex operational requirements limit adoption compared with electric tools.

Other modes of operation represent 14.9% of the overall market share, including hydraulic and engine-driven power tools used mainly in industrial and outdoor applications.

Application Analysis

The industrial/professional application segment holds the largest position in the power tools market, contributing 68.0% of the overall market share. This dominance is driven by extensive usage across construction, automotive, manufacturing, aerospace, and other heavy industries. The construction industry contributes 14.0% due to rapid infrastructure development, urbanization, and commercial and residential construction activities.

The automotive sector contributes 6.0%, while manufacturing applications account for 5.0%, supported by increasing vehicle production, assembly line automation, and industrialization.

The residential/DIY segment contributes 4.0%, benefiting from rising home improvement activities and easy availability of affordable power tools. The aerospace industry contributes 1.5%, while remaining applications account for 1.5% of the market share.

Distribution Channel Analysis

Offline retail remains the leading distribution channel, accounting for approximately 58.0% share of global power tools revenue. Hardware stores and specialty distributors continue to attract professional contractors and industrial buyers due to physical product evaluation, immediate availability, technical assistance, and warranty support. Construction contractors commonly purchase tools such as rotary hammers and impact drivers through authorized dealers offering demonstrations, training, and maintenance services. Manufacturing companies also rely on offline networks for specialized tools requiring technical guidance and customized procurement agreements.

Meanwhile, online retail is experiencing steady growth due to expanding e-commerce platforms, competitive pricing, wider product availability, improved delivery services, digital procurement, and increasing DIY adoption.

Key Market Segments

By Tool Type

- Drilling and Fastening Tools

- Sawing and Cutting Tools

- Demolition Tools

- Material Removal Tools (Grinders, Sanders)

- Wrenches

- Routing Tools

- Others

By Mode of Operation

- Electric

- Pneumatic

- Others

By Application

- Industrial/Professional

- Construction

- Automotive

- Manufacturing

- Aerospace

- Residential/DIY

- Others

By Distribution Channel

- Direct Sales

- Offline Retail

- Online Retail

- Others

Driving Factors

Infrastructure development and construction investments across emerging economies represent major growth drivers for the professional power tools market. India’s construction output is expected to increase by as much as 4.4% in 2026 after achieving 7.4% growth in 2025. This expansion is supported by government capital expenditure of nearly INR 11.1 trillion and approximately USD 134 billion allocated toward infrastructure projects covering highways, airports, metro systems, and industrial corridors. Such investments can create a 1.3–1.7 times multiplier effect on demand from construction-related trades.

The Middle East is also experiencing a major investment cycle, with the regional power tools market valued at USD 1.5 billion in 2024. Development initiatives including Saudi Vision 2030, the UAE’s AED 4.5 trillion long-term development pipeline, and ongoing urban maintenance requirements in Qatar are supporting regional demand. Global construction output is forecast to grow by 2.3%, with emerging markets expanding by 3.1% compared with 1.5% in advanced economies.

Additional growth drivers include cordless and brushless motor technology adoption, residential renovation trends, industrial automation, battery technology advancements, and e-commerce expansion.

Restraining Factors

Raw material price volatility remains a major challenge for the power tools industry. Steel prices increased by 8.2%, while aluminum prices averaged 10% above earlier benchmarks. These materials account for approximately 45%–55% of the bill of materials for standard corded or pneumatic tools.

Cordless tool manufacturers also face cobalt supply risks, as nearly 70% of global cobalt production originates from the Democratic Republic of the Congo.

In June 2026, rising energy and logistics costs linked to the Iran conflict added further pressure across battery mining, refining, and manufacturing operations. Current input inflation could reduce gross margins by 4.5–5.5 percentage points before mitigation measures are implemented. Price increases remain difficult in the USD 40–120 entry-professional category, where low-cost Asian suppliers maintain competitive advantages. Manufacturers may absorb 50%–65% of higher expenses.

Risk mitigation strategies include procurement contracts covering 6–9 months, redesign programs reducing metal usage by 10%–15%, and adoption of premium brushless and connected tools capable of passing through 70%–80% of additional costs.

Growth Opportunity

The tool rental and Equipment-as-a-Service model represents a major growth opportunity in the power tools industry. The broader equipment rental market was valued at approximately USD 240.58 billion in 2026 and is projected to reach USD 411.55 billion by 2035, expanding at a 6.16% CAGR.

Dedicated subscription platforms for SME contractors, independent tradespeople, and urban DIY consumers remain underdeveloped. Professional cordless drills priced at USD 350–450 could generate USD 180–240 annually through a USD 15–20 monthly subscription model. An OEM-operated platform combining connected fleet management, maintenance services, and accessory cross-selling could achieve gross margins of 55%–60%, compared with 38%–42% from conventional hardware sales.

Additional opportunities include smart and IoT-connected tool ecosystems, untapped DIY markets in APAC and MEA, AI-integrated predictive maintenance platforms, green and circular economy tool re-commerce, and M&A expansion of regional mid-market brands.